SWIFT - What Actually Is It??

Hey Guys,

It’s been a while. I hope you’re all doing ok in these choppy markets, and with everything that is going on in the world.

This one was a bit late as I’ve had a busy few weeks in both personal and work life.

Went to the dreaded Pryzm in Cardiff for my sister’s Birthday a few weekends ago, and actually had the time of our lives, then came down with a cold, and I didn’t have any Wi-Fi last week. Tragic.

Anyway, this week I decided to take a little dive into what SWIFT actually is, as you’ve probably heard the news that some Russian banks have been removed from it.

I also have another excellent podcast. This time with Mr Zucc.

As always, if you can think of anyone who would find this useful, please share this newsletter with them, using this juicy button:

And they can subscribe here:

SWIFT vs Bitcoin

Society for Worldwide Interbank Financial Telecommunication - SWIFT, what does it actually do?

As I’m sure a few of you know, SWIFT is an international payment network used by banks and institutions, which is currently playing a part in the retaliation against Russia - specifically, the exclusion of several Russian banks from the network.

Despite what you may intuitively think, SWIFT does not actually send any money. It is not a bank, or a clearing house, or settlement institution, and does not manage or hold any funds. SWIFT is in fact a messaging network, which allows banks to communicate with each other.

Prior to SWIFT, they had to use Telex. Telex was pretty shit. Senders had to describe the transactions in sentences that were then executed and interpreted by the receiver. Naturally, this led to many human errors as well as slow processing times.

To circumvent these problems, in 1973, a cooperative society with 239 banks from 15 countries, was formed to operate a global network to transfer financial messages in a more secure and timely manner - SWIFT.

It was a huge success, processing more that 10 million messages in 12 months, and today it is used by over 11,000 institutions from over 200 countries. Its success can be attributed to the fact it made cross border payments faster, more secure, and much simpler.

Instead of sentences, a standardised code was created to help describe transactions.

For instance, SWIFT assigns each financial organization a unique code that has eight or 11 characters. This code is either called the bank identifier code (BIC), SWIFT code, SWIFT ID, of ISO 9326 code. There are 4 parts to the code, they represent the institute code, country code, location/city code, and an optional part which is used by organizations to assign code to individual branches.

So, what happens if Will in the UK wants to send money to Matilda in Brazil?

Like all the best thing in life, there is a cost…

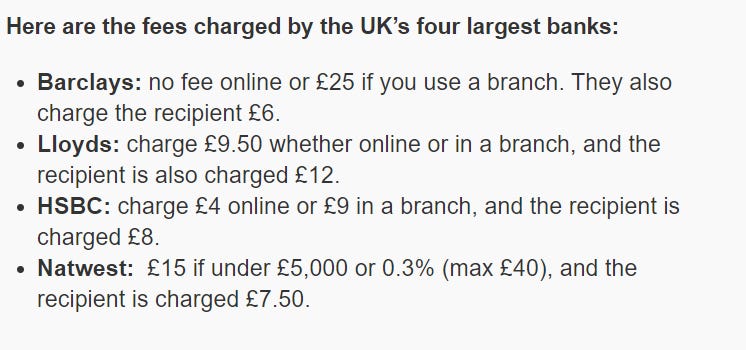

The first is a simple fee, you can see the charges for the main UK banks below.

But that’s just a teaser, the greatest cost comes from the exchange rates. Allegedly there is approximately a 3-4% exchange rate margin, however this is only from one source, so I checked with Lloyds bank. The exchange margins range from 1.4 - 3.55% depending on the size of the transaction, so I think this is in the right ballpark.

For a transaction of £10,000, it will be 3.55% with a £20 fee as this payment is not to the USA, Canada or Europe, totalling £375!

You will need to provide the personal details of yourself and your friend, as well as their banks address and the SWIFT code of the bank they use.

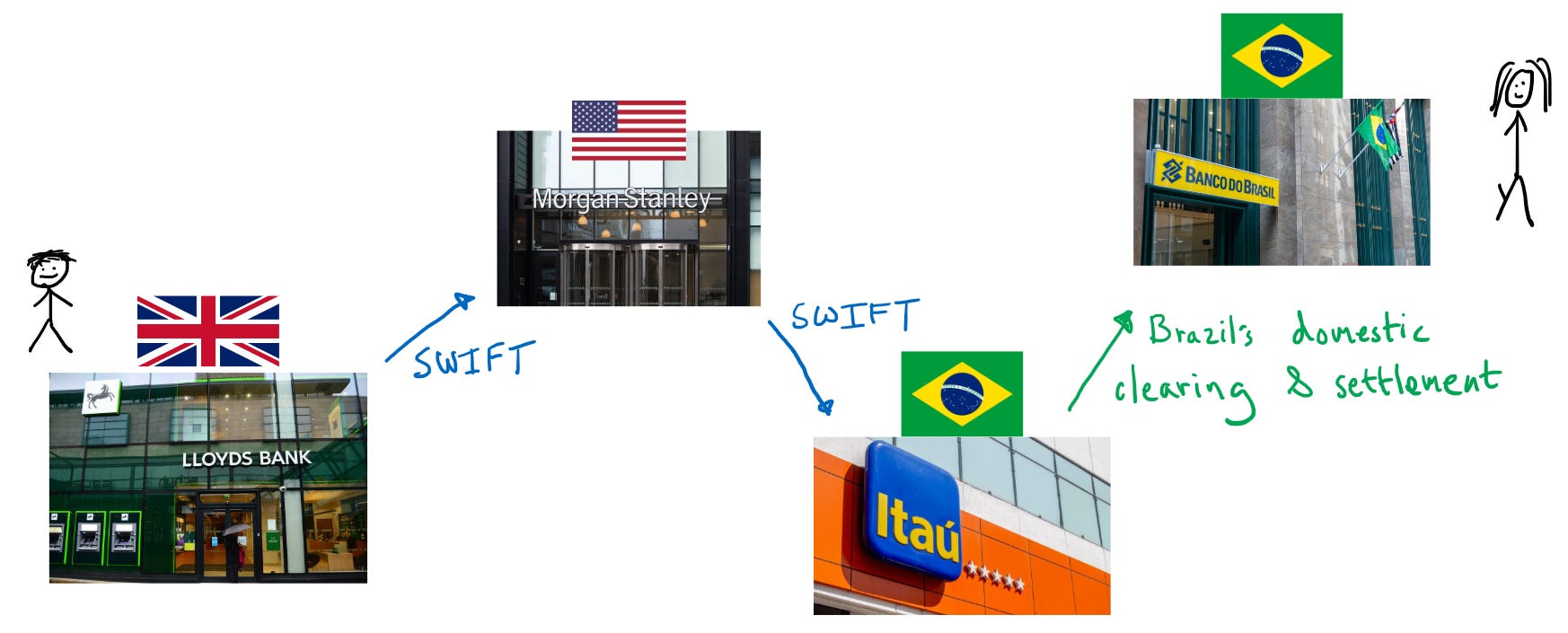

Assuming you got all the details correct, a SWIFT message will then be sent. However, unless Will’s bank has a correspondent account with Matida’s account, the bank cannot directly send the message to Matilda’s bank.

A correspondent account is an account established by a bank, to receive deposits, make payments, or handle other financial transactions for another bank, usually in another country. So, a Lloyds customer in the UK can send a transaction to a friend in the USA without needing to have a Lloyds bank in the USA.

However, many banks do not have direct correspondent banking relationships, especially if one of the banks is in a less developed country. In this case, the transaction needs to be routed through an intermediary bank/banks which are connected through a corresponding banking relationship.

This is why the fee for the Lloyds transaction is £20, not the £9.50 seen above because for every intermediary bank the payments have to go through, there is another cost.

For example, the payment is routed to a US bank, who does have corresponding banking relationships in Brazil, then send to the Brazilian bank Itau, as they don’t have a direction relationship with Matilda’s bank. Finally, the transaction reaches Banco do Brazil through Brazil’s clearing and settlement system.

And this is only one possible path, there may be other faster or cheaper paths and choosing one is trade-off, between speed and cost. Each bank is a point of failure, with additional fees, and it’s the cause for transaction delays and failures.

Back in 2018, Ripple Labs CEO, claimed:

“SWIFT’s published error rate is six per cent. Now, I will talk to corporate treasury people and they will actually tell you it is higher than six per cent but even the six per cent….”

However, this is in fact a false claim, based on misinterpretation on a paper released by SWIFT themselves. There is in fact a 100% guaranteed delivery of SWIFT messages and the error actually arises from the banks and middlemen. This is in part due to varying exchange controls, anti-money laundering checks, and information errors. Even when these errors are detected, usually by the recipient who hasn’t received the money, it is no easy task to go back through the transaction path to try and find at which bank the error occurred or whether it is simply due to the sender inputting the incorrect data.

These are the words of Sir Jon Cunliffe, Chair of the Committee on Payments and Market Infrastructures (CPMI),

“it can still take as long as 10 days to transfer money to different jurisdictions. And that transaction can cost up to 10 per cent of the value of the transfer. A payment from the UK to some countries has to go through four currencies and as many as five banks.

It’s a bit of a mess. This is a system formed and used by institutions, which has been around for almost 50 years. Despite 50 years of innovation and improvement of the network, it can still take days with high costs just to send some money abroad. This seems to be a bit of a dinosaur in a world where you can send messages, to anyone anywhere in the world, instantly and free, and is clearly in need of improvement.

Part of this improvement may come from CBDC’s (Central Bank Digital Currencies), and new fintech companies like Ripple.

But isn’t one of the most obvious ways to solve this problem, just to have a global money? If a money is borderless, the problem of cross border payments simply disappears. This doesn’t mean you can’t have other native currencies, but the very existence of such a money would make it much easier for anyone to send money abroad and make much of the current infrastructure for cross border payments, irrelevant.

This is basically what we have with Bitcoin. It’s not perfect, but you can send transaction faster, cheaper and more securely… The very same reasons why SWIFT was a huge success compared to Telex.

And as Jack Mallers fabulously demonstrates with some tortilla chips, raisins, and peanuts (see below), you can build infrastructure around Bitcoin, for example payment apps like Strike and Cash app, in which you don’t even need to own any Bitcoin in order to use the network.

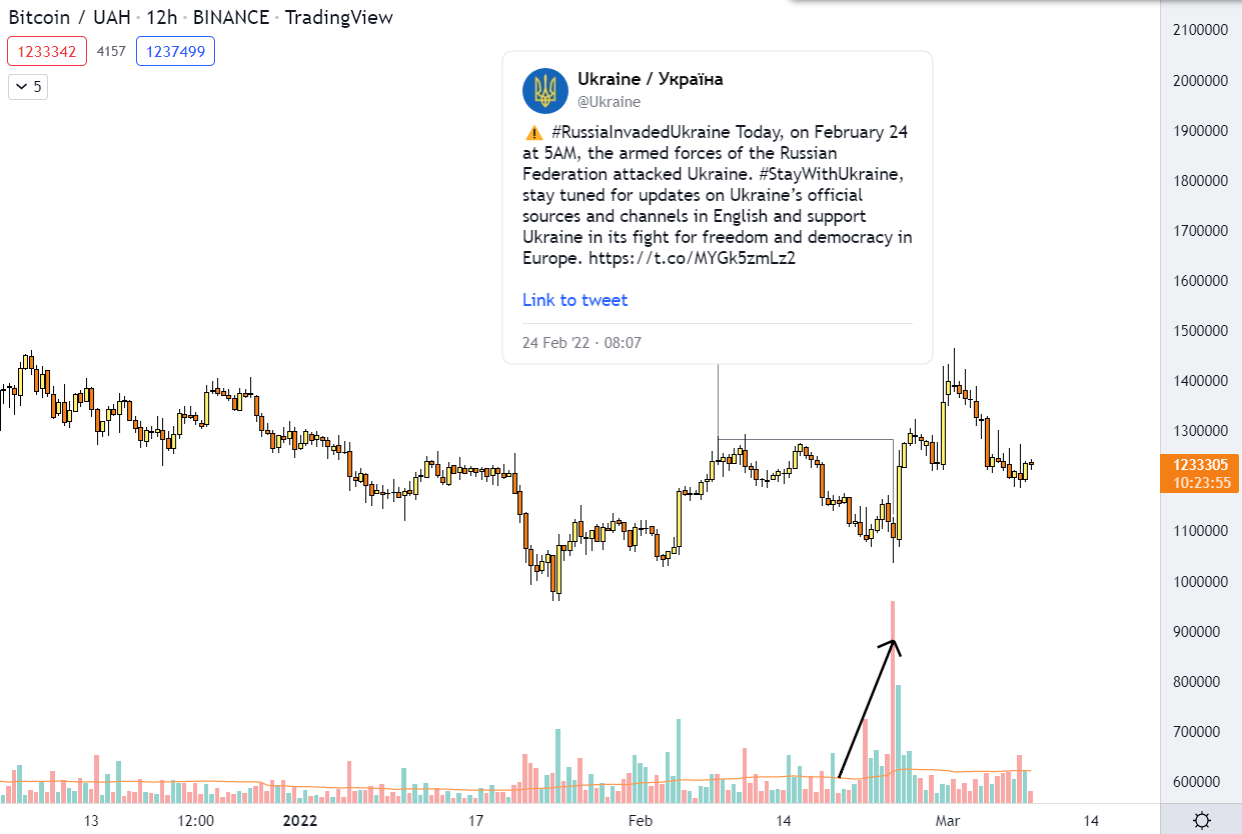

The current conflict in Ukraine is also highlighting the ease and simplicity of Bitcoin as a payment system. Here is a post by the Ukrainian Government just after the invasion:

They did not post a bank account number. They posted a Bitcoin and Ethereum address which anyone anywhere in the world can send money to.

They have since raised over $50 million from crypto donations, of which $15 million has already been used to buy military gear, all within a matter of days.

In contrast, Peter Schiff’s gold donations will allegedly be arriving in a few months.…

Beginners

If you had watched the video in last week’s section, you should now have some sort of understanding of how Bitcoin works. This week you can dive deeper into the bullish case for Bitcoin along with some of the possible risks. The following is the audio version of the book, ‘The Bullish Case for Bitcoin’, by Vijay Boyapati. It’s not too long and covers most of the aspects surrounding Bitcoin.

"It may seem foolish to invest in a digital asset that isn’t backed by any commodity or government and whose price rise has prompted some to compare it to the tulip mania or the dot-com bubble. Neither is true; the bullish case for Bitcoin is compelling but far from obvious. There are significant risks to investing in Bitcoin, but, as I will argue, there is still an immense opportunity." - Vijay

You can also read the original article the preceded the book here.

Bitcoin

It’s been a pretty turbulent time for all assets, with the stock markets crashing and commodities rocketing. This is bad environment for all risky assets, including Bitcoin. However, we are also seeing some of the reasons as to why many Bitcoiners, view Bitcoin as a safe haven asset.

Trading volume for the Bitcoin/Hryvnia (Ukraine’s currency), and the Bitcoin/Ruble pairs on Binance both spiked around the time the invasion began.

This is especially visible on the Russian Ruble pair which has had sustained volume growth as Russian civilians look for alternatives to help preserve their wealth as their native currency crashed and stocks went into freefall.

Here is the Ruble and the Russian stock market against the dollar. The Ruble is down around 40% and stocks over 70% since the invasion:

Pretty scary for civilians in either of those countries. In an environment where the Russian central bank has blocked civilians from buying any dollars (with the Ruble), Bitcoin and stablecoins are a lifesaver.

Touching on a similar topic, here is a brief section on Bitcoin, from Lyn Alden’s newsletter, which I recommend you subscribe too:

It’s still too small and volatile for most sovereign entities to want to hold it, but it can serve well as “people’s money”. Ukrainians facing ATM freezes and such? Having self-custodied bitcoin or gold helps with that (and Ukrainians are ranked #4 on the crypto adoption index, meaning they have a very large per-capita holding of bitcoins and crypto compared to other countries). Russians facing a tanking currency and stock market? Well, gold and bitcoin are both at all-time highs in ruble terms, so people holding them have held up well compared to most of their peers (and Russia is #19 on the crypto adoption index). People living in any of the dozens of countries (representing roughly a billion people) that are currently experiencing official double-digit inflation? Again, things like gold and bitcoin are an option for them to try to protect their savings, especially because buying foreign stock indices is not always as easy to do, and those assets can be confiscated/frozen by their governments in a currency crisis anyway. Not everyone can afford a house, which is the most common form of inflation protection.

Price

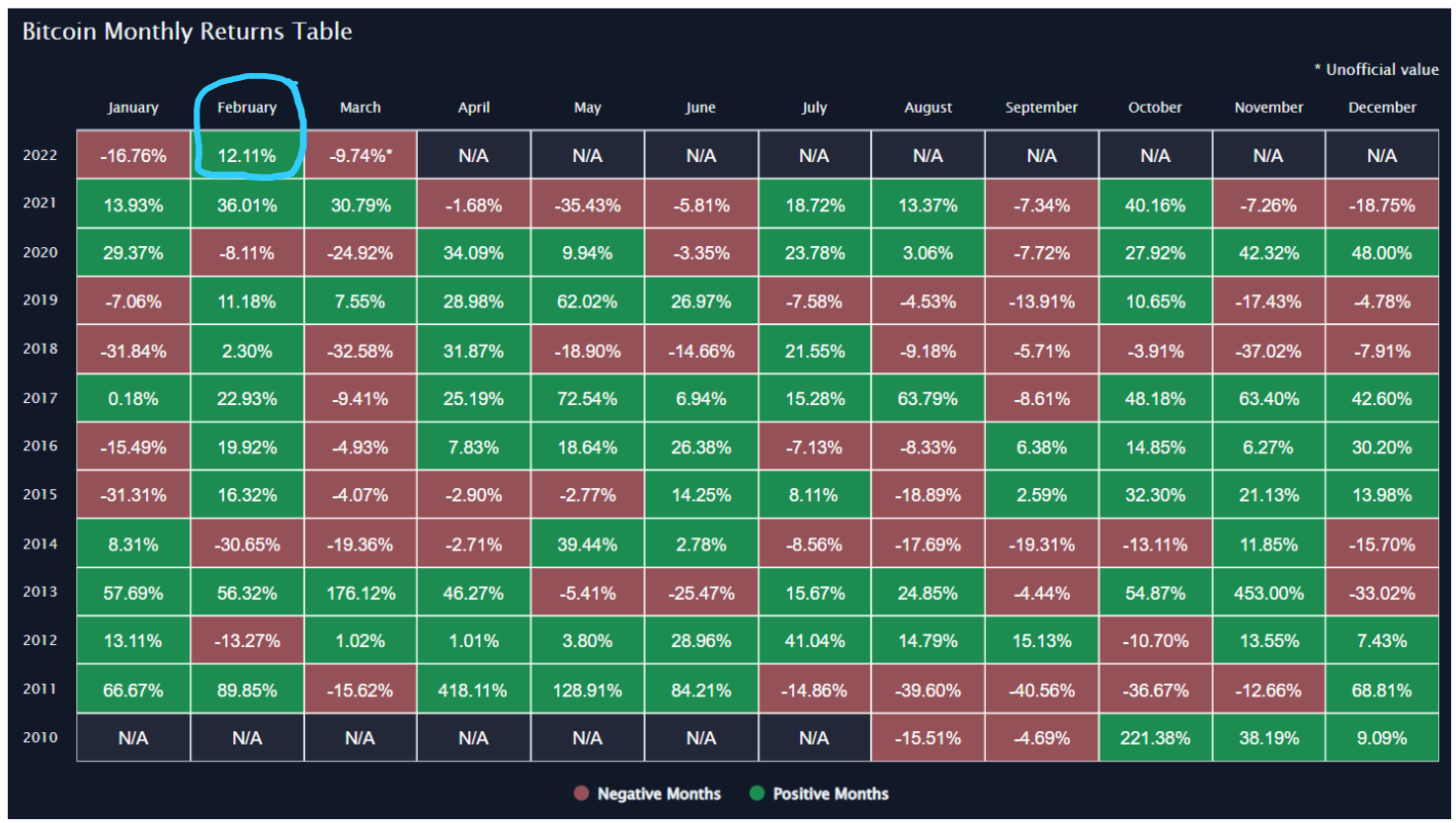

As for the Bitcoin price, the relentless downtrend that it has been in for the past few months has taken a bit of a pause, and February even ended with double digit growth, closing at 12.22%.

Bitcoin recently broke out of its trendline but is currently fighting to get above the 45k area, which coincides with the bull market support band. Where we go from here is anyone guess. The trend remains down, but the momentum is slowing, which is a sign that the strength of the bears is potentially weakening.

The main task for Bitcoin remains to get above $45k and the bull market support band.

Whether we breakout or not, the overall picture remains the same: We are still in a range from $30-$60k and until we go back into a more risk-on environment, it seems unlikely that Bitcoin will be making all-time highs anytime soon.

Looking On-Chain and to the Stock Market

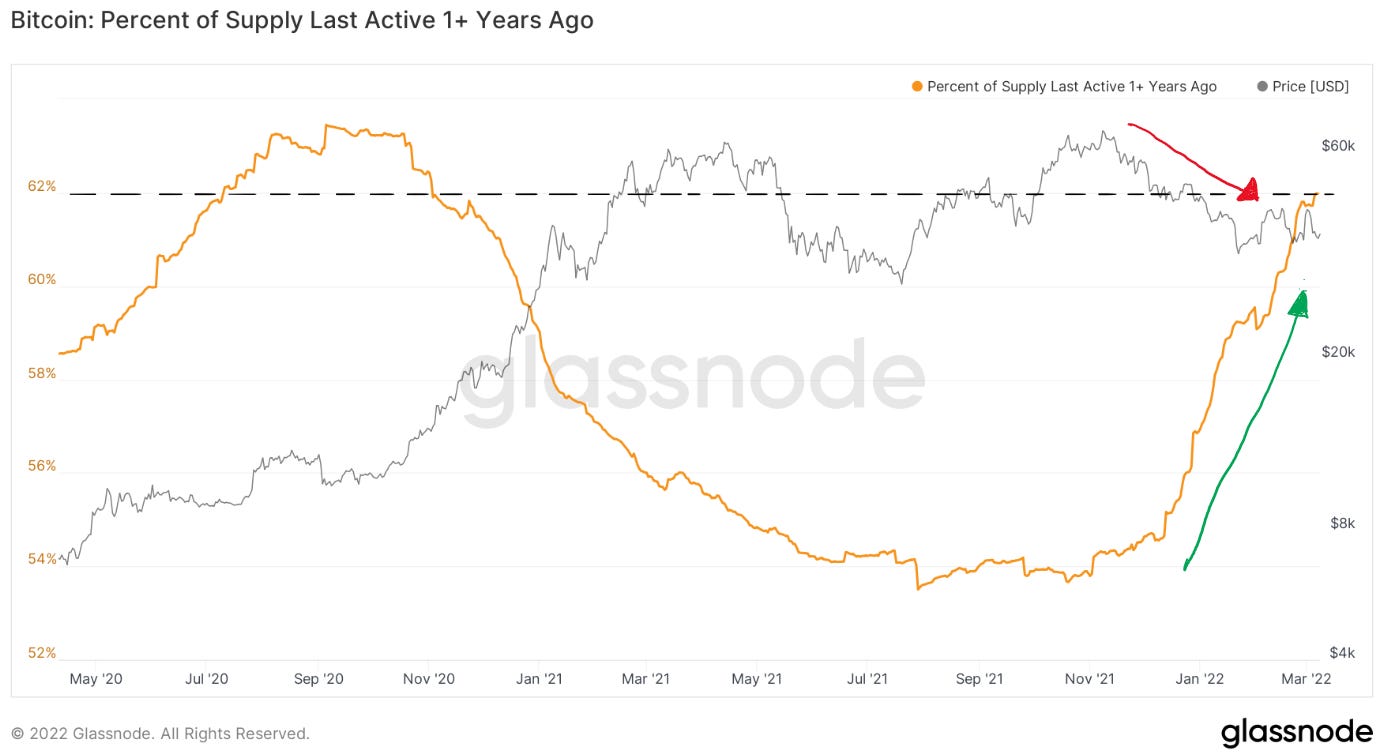

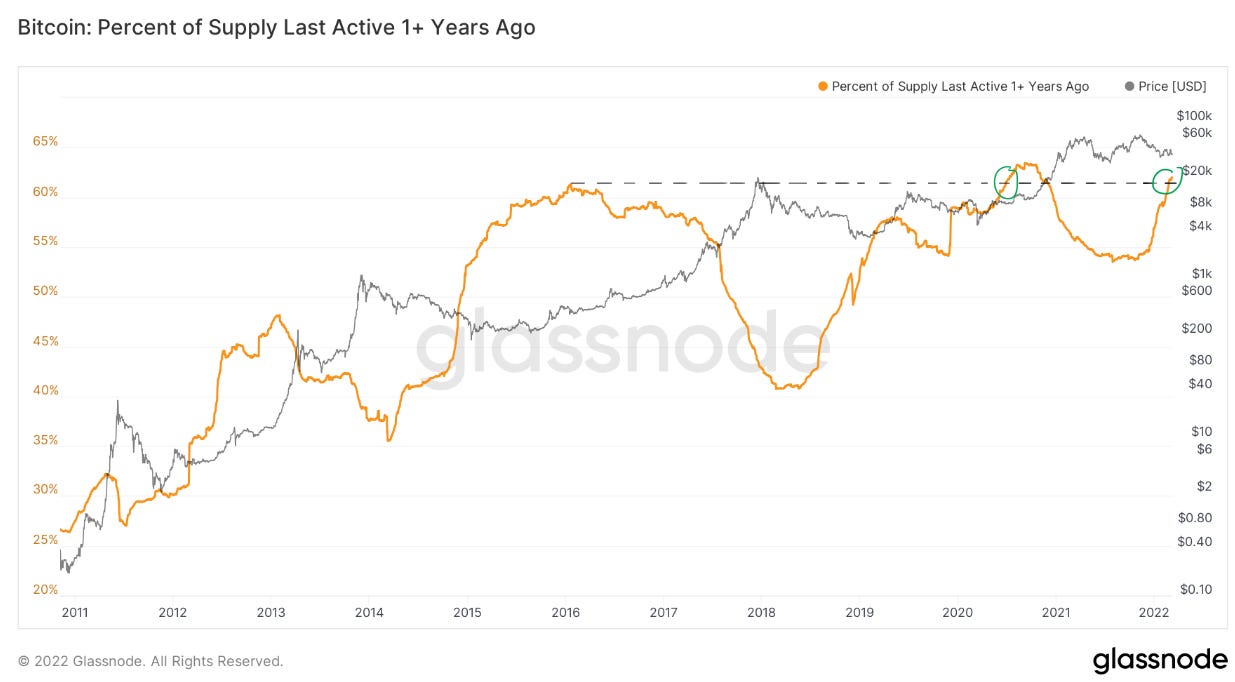

There is an interesting is the divergence between the price and the supply last active a year or more ago. In the last 3 months, the price has been falling, yet the amount of supply being ‘hodled’ for over a year has been increasing dramatically.

This shows that despite all the volatility we’ve seen over the last year, 62% of coins have not been or sold or moved, and this continues to rise in a sharp uptrend. This adds to the thesis, that the supply side of Bitcoin remains pretty tight.

If we zoom out, we can see that there have only been two other times when supply has been this tight, at the start of the 2017 and 2021 run up. The only difference this time, as discussed in the last newsletter, is that the demand is missing.

I continue to see this as an excellent opportunity to DCA slowly in. It’s possible we crash lower, but if you DCA over at least the next 3 months, you’re quite likely to catch the bottom. Please note though, that if we do get a capitulation crash and Bitcoin crashes down $20k, you want to have some cash ready to take advantage of such an opportunity. Prepare for all scenarios

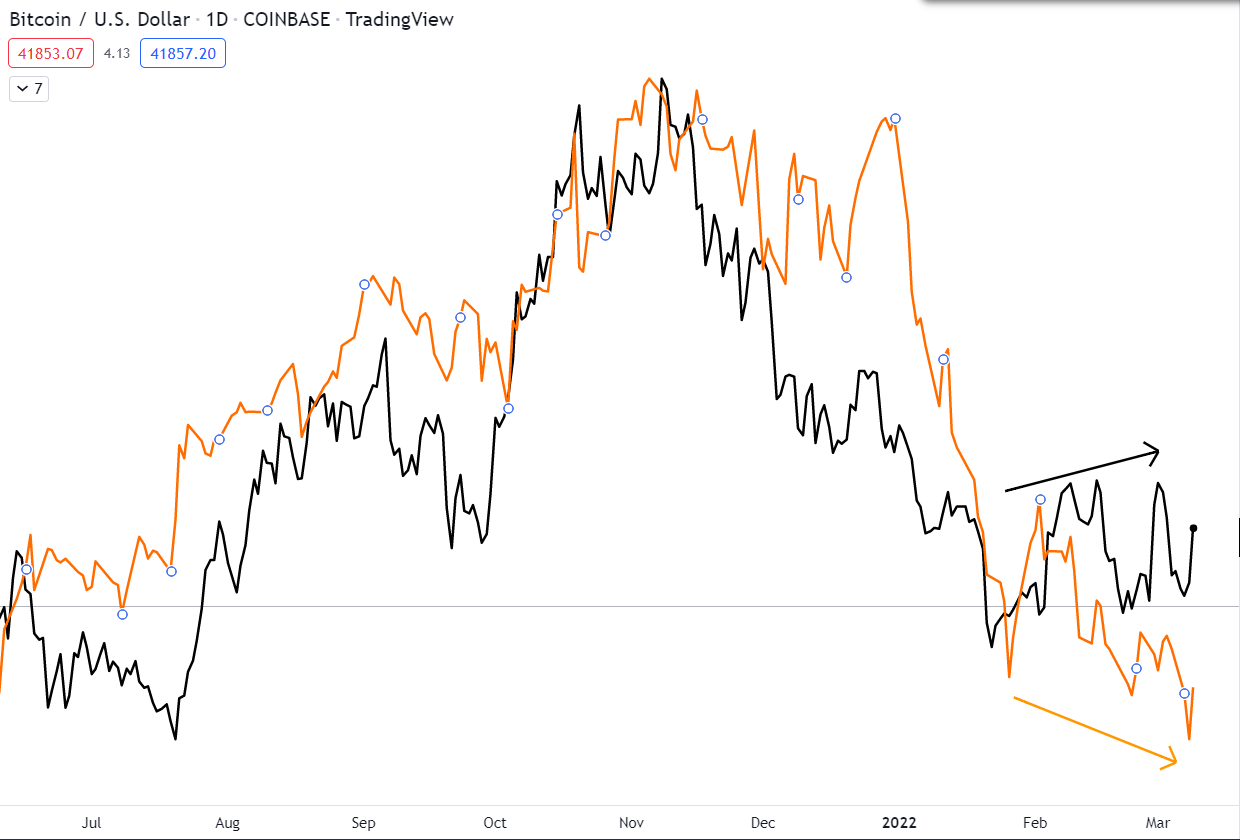

Another interesting divergence is between the Nasdaq and Bitcoin. Up until now the two have been very correlated. This is because tech stocks make up over 50% of the Nasdaq, so it acts as a risk-on asset, like Bitcoin.

Below you can see the Nasdaq in orange and Bitcoin in black.

Ever since early February, Bitcoin has started rising up whilst the Nasdaq continues to fall. This shows relative strength in favour of Bitcoin and is something we would like to see more of moving forward, especially in this risk-off environment.

On similar note, here in an interesting chart, which shows Bitcoin denominated by the Nasdaq (Bitcoin/Nasdaq). What we see is a history of sideways chopping action, in form of a flag, followed by a decoupling/breakout, which happens when Bitcoin goes parabolic. What we see is that we have been in a similar wedging pattern to 2017, just less volatile, and if the same thing plays out, we could see a breakout within the next year. An uplifting bit of dubious speculation.

Pick of the Week

A lot has happened in the last few weeks with regards to crypto fundamentals, one of the biggest events was the Swiss city, Lugano, making Bitcoin legal tender. Yet another step on the ladder for the general adoption of Bitcoin on a larger scale.

Personal

Podcast Recommendation:

Mark Zuckerberg on the Lex Fridman Podcast

I’ve never been a fan of Zucc, and quite frankly I’ve always seen him as a bit of an alien. A slightly dangerous alien. But this podcast has definitely opened my eyes and reminded me, once more, not to judge so quickly. Lex ask’s some very direct questions, along the lines of, “How does it feel to know so many people hate you”, and it’s nice to hear a more human side to Zucc as he responds to such questions. Of course, I’m sure he was well advised on what to say and not to say, during such a big podcast, but it definitely felt like there were hints of a truly genuine caring human in there.

Article Recommendation:

Essential Life-Learnings from 14 Years of Brain Pickings

A beautiful little article shared by Tim Ferris which I thought I’d pass on to you guys.

Well done for getting this far and continuing to learn about money and the world of Bitcoin with me. It’s more important than ever to be educated on these things as we are now witnessing currency being increasingly weaponised at an unprecedented scale.

Don’t make any silly decisions out there, and I hope you have a wonderful week.

All the best,

Tats