What is actually going on?

The things you need to understand.

I recently met up with a good friend of mine who has been on a work placement in Germany. He’s a bright guy with a passion for chemistry. He once matched with a girl on tinder, who lightly asked why it was that camomile tea made you sleepy. Without thinking, he proceeded to write an essay on the chemical properties of chamomile and why it produced the side effect of sleepiness, then sent it to her. Unfortunately, she was not the one, and he never heard from her again.

(Don’t worry, he survived.)

Aside from his love of chemistry, he also has some desire to learn about finance, as he struggles a bit with his personal budget. He is an avid reader of my newsletter, and as we reunited at the Gallimaufry pub in Bristol, he said to me, “Tats. I love your newsletter and have read every single one. But I still have absolutely no idea what’s going on.”

It was funny at the time, but later it made me wonder how many other people are reading this newsletter with a desire to learn, grasping things here and there, but still not truly understanding the bigger picture of where the world finds itself today.

So, in this edition I’m going to touch base. I’m going to try and explain the current macro environment as simply as possible.

In addition, I will touch on ways you can protect yourself financially in such times, a brief overview of the recent crypto carnage, and a quick update on Bitcoin.

Before we dive into things, a quick announcement!

Part of the reason this newsletter has gone from weekly, to fortnightly, and now monthly, is that I’ve been working hard with the Do Lectures to try and create a special 3-day blockchain festival covering all key aspects of Bitcoin and crypto.

I had my doubts at the start, as the challenge of bringing world-class speakers from the US and Europe to a small CowShed in Wales seemed pretty far-fetched. However, after reaching out to well over 70 speakers, I can proudly say we have a pretty stellar line-up. Speakers won’t just be talking, they will also be holding interactive workshops and staying on the farm for the whole 3 days.

You sleep in tipi tents. There’s live music. A barista making freshly ground coffee. And best of all, there’s a crowd of curious people.

I think it’s going to be pretty special.

The event will be on the 11-14 of May 2023. Tickets are not out yet, but you can register interest at: cowshed.org.uk

And you have until Friday to be able to win a free ticket! How to win FREE ticket.

I’m going to try and make this as accessible as possible, so all ‘funny’ finance words will be put in bold and explained in italic writing.

Now, let’s dive in.

A bank has two sole purposes. To hold your deposits (money) safely and to invest it for you. Keeping all your money on you is not very convenient and there is a risk you can get robbed. An institution that invests a lot of money in security, can protect your money much better than you can, and will take a small fee in return. In addition, a bank can invest money on your behalf, because they can have a specialised team of analysts and investors who will invest your money, and once again take a small fee in return.

Both of these services are extremely useful and its why banks came to exist.

Back in the good old days, gold was used as money. Gold is good at keeping its value over time, as you can only increase the supply by so much every year - a limited supply. However, gold is extremely difficult to transport over space. The further through space you have to send gold and the higher the value of the payment, the more expensive it is, in part due to the weight, but also because you need to invest more in security.

As the world became more globally connected, it became very convenient just to deposit your gold at a bank and in return be given some paper which was your claim on that gold.

A paper claim was simply a piece of paper that was proof of your ownership of a certain amount of gold that you deposited at the bank. This then evolved into paper currency, which is paper money (like cash notes today) given out by the government, except these cash notes could be exchanged into a specific amount of gold at the bank. This gave the currency credibility and is the basis of ‘the gold standard’.

Knowing that there was a low probability that everyone would pull all their gold out at once, the banks started issuing more paper claims on the gold than the amount of gold actually held in their vaults, and they would then invest that extra money in long-duration less liquid assets.

Long-duration means that the maturity date is well into the future. So, a 30-year government bond will pay interest until the 30 years is up and it has ‘matured’. Short-duration would be more like a 1-month bond which ‘matures’ after one month of being issued. Less liquid means it is harder to sell. Cash is the most liquid assets, because you can ‘sell’ it in return for pretty much anything very quickly. A house on the other hand is not very liquid, because it’s much harder to sell into cash. A bond is simply a promise by a borrower to pay back the money along with some interest over a specified duration of time.

This system of issuing more loans than the amount of money you actually have is called ‘fraction reserve banking’ and is used all around the world today.

Back in the early 1900s, bank runs were a common occurrence. If people suspected that banks were doing dodgy dealings, everyone would go to withdraw their gold, and if the bank didn’t have the gold to meet the withdrawals, they would go bankrupt and in effect be ‘punished’ for their bad risk management and greediness. A bit like we are seeing in crypto today with Celsius and FTX.

However, to try and stop the number of bank runs, the central bank was created to act as a lender of last resort, so that banks could meet their obligations (money they owe and need to pay back) when they had no money left. However, this incentivises banks to be riskier than they usually would be, as they now have a safety net.

The other role the central bank plays are providing money to the government when the government needs funding.

It should be noted that whenever the central bank buys assets or lends money, it does so by magicking the country’s currency out of thin air.

Generally, a government in need of funding can take on debt by issuing bonds. However, if no one wants to lend the government money (buy the bonds), the government faces bankruptcy. The government then turns to the central bank, who prints money to buy the bonds from them, lending them money. Central banks buying government debt is called ‘debt monetisation’, and the result is an increased supply of the currency and greater government debt in the system.

Remember, a government bond is a promise that the government will pay back the value of the bond with interest sometime in the future depending on the type of bond. 30-year bond means the value is paid back in 30 years with interest being paid every year.

What we have just covered, is two ways in which the amount of currency in the system can increase.

The first is that private banks can issue more paper claims on gold than they actually hold. So, if a bank holds £20 million in gold, they might actually issue £30 million in paper claims on the gold.

The second method is that the central bank can print money to bail out banks in distress, as a lender of last resort, and also to governments, by buying government bonds when the government is in need of funding.

One scenario in which governments are always in need of funding is during war, as wars are bloody expensive and can’t be paid for by tax alone. Central banks have no choice but to print and fund the war budget by buying government bonds, as the central bank is ultimately a branch of the government that must bend to its will in times of crisis, similar to Covid. During both world wars, more paper currency was issued than there was gold, so there were periods when governments closed the gold standard and said you could not exchange your paper currency for gold, and when you could, it was for less gold than you initially put into the bank.

For example, imagine you put £50 of gold into a bank and get £50 worth of paper currency in return, with a promise that you can exchange it for a specific amount of gold. Then, following a period of extreme money printing, when you go back to exchange the £50 for the same amount of gold, you in fact get less in return as they have devalued the paper currency and naughtily broken the promise.

This is essentially a sovereign default. If you were holding a paper dollar or a paper pound based on the promise that it was redeemable for a specific amount of gold, and then the government overnight said that it’s either not redeemable, or redeemable for less gold than before, then they unilaterally broke the contract.

This was one of the problems with the gold standard. Governments couldn’t help issuing more currency than their gold holdings, especially during times of crisis, and so a sovereign default of this type was not so uncommon.

Heading into the late 1960s, there was once again more paper claims than there was gold and the global monetary system started to break down. Once again, the US government defaulted, and took the dollar off the gold standard and dollars were no longer redeemable for gold. All other governments followed suit and we ended up in the fiat system we live in today.

Fiat means that the currency is not actually backed by anything.

All currencies in the world today are not backed by anything ‘hard’ like gold, so all governments have the ability to print as much money as they desire. This has resulted in numerous developing countries having hyperinflation, whilst developed countries have managed to survive with a fairly steady amount of inflation, so far.

By hard I mean something in which the supply is limited.

This steady inflation is essentially a hidden tax on savings, as people work to earn a currency, which is devaluing every year due to printing.

One of the other consequences of the fiat system, is that governments in developed countries have been able to get away with being very unprofitable, because they are able to issue more debt (sell bonds) to make up for any losses. This is because cash savings are generally not ideal as they are being constantly inflated away, so holding your savings in government debt becomes rather attractive as it offers a yield. For example, UK pension funds, foreign governments and individuals will buy UK government debt (bonds). In addition, when there are still not enough buyers for the debt, i.e. during a crisis like Covid, the central bank can just step in and buy it instead. The cost of the central bank doing this is once again people’s cash savings being further inflated away.

There is no initial problem with this dynamic. However, as the government continues to borrow more to finance their deficit, their debt can become so large that financing that debt (paying interest) can actually start to become a significant portion of their annual spending. This will increase the deficit further, leading them to borrow further, which can land them in a very dangerous debt spiral that they do not want to end up in.

Deficit is the amount they are losing in money each year. Tax Income - Spending = Deficit

We can see this government unprofitability by looking at the deficit as a percentage of GDP.

Gross domestic product (GDP) is a measure of the value of all the final goods and services produced and sold over a specific time period by a country. GDP can be thought of as the government’s ability to generate income. The greater the GDP, the greater the tax income. Looking at the deficit in pounds of dollars doesn’t give a good measure of the deficit, because those pounds and dollars are decreasing in value over time. A deficit of £100 million today, is much smaller than a deficit of £100 million 50 years ago. Therefore, if we look at the size of the deficit/GDP this tells us how much the government is losing money, relative to its ability to make money.

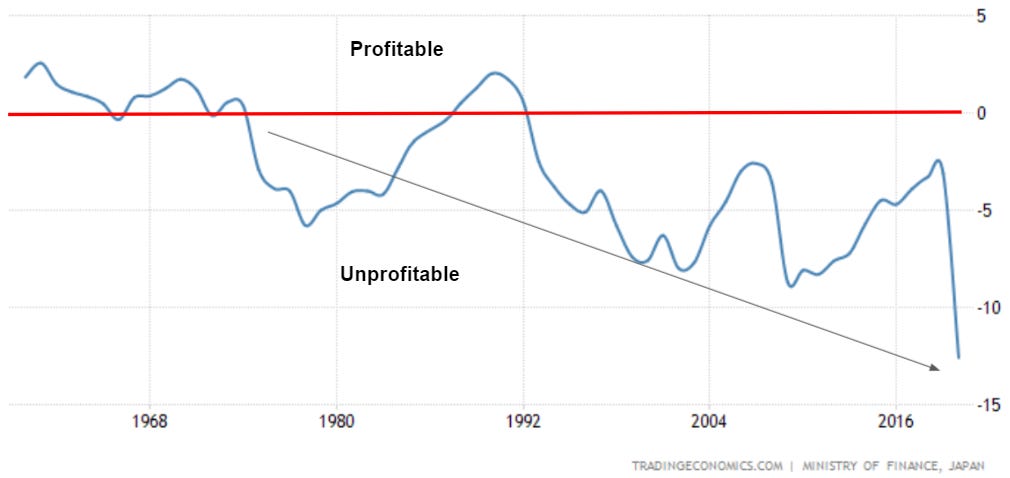

Japan’s Deficit:

UK’s Deficit:

US’s Deficit:

As you can see, these are turning into some pretty mighty deficits. If these deficits are funded by debt, your next question should be what the government debt for these countries looks like.

Once again, let’s look at the government debt by dividing it by GDP, as it gives the debt as a proportion to the government’s ability to make money.

Japan’s is by far the worst. Following the crash of one of the greatest bubbles in history, Japan has been trying to stimulate its economy and has ended up with the greatest debt-GDP ratio in the world.

The UK is also pretty bad at near 100% debt-GDP, but it pales in comparison to what they had following WW1 and WW2 when they had up to 250% debt-GDP.

Following the Covid and the 2008 Great Financial Crisis, the US finds itself at levels not seen since WW2, with 120% debt-GDP.

Now, for anyone with a lot of debt, be it a mortgage or a business loan, the first thing you should ask is what’s the interest rate. The only way for an individual to have a mortgage many multiples greater than their annual income, is if the interest rate is very low. Given that governments control interest rates through the central bank, what do you think interest rates have been doing whilst debt-GDP has been rising since the 70s.

Down, down, down, do…. up?

In this chart I have plotted the yield of the 3-month treasury bill (red), as its historical data goes back the furthest and it tracks the general interest rate of the Federal Reserve (US central bank) very closely. In addition, I have also plotted the debt-GDP (blue) we looked at above, so we can see the relationship.

As you can see in the chart above, when debt-GDP is increasing, interest rates tend to be falling, and as debt-GDP is decreasing, interest rates are rising. Quite simply, when debt-GDP is over 100%, governments can’t afford to let interest rates increase too much for too long, and vice versa.

Debt-GDP has been growing steadily for the last four decades and interest rates have been falling.

Until this year.

What we are seeing today, is the federal reserve hiking rates at record pace whilst debt-GDP is well over 100 percent!

There are a few clear questions one should now be asking:

How did countries previously get their debt-GDP ratio’s down from the highs in the 40s following WW2?

Why is the Fed raising rates so much when debt-GDP is this high?

Can governments afford to raise rates when debt-GDP is so high?

What does this all mean for the average Joe?

Let’s dig in.

The answer to the first question can be found in a paper published by the International Monetary Fund back in 2015 called The Liquidation of Government Debt. I’ll show you the abstract, and then we will make sense of it.

Here’s the abstract of the 2015 IMF paper:

High public debt often produces the drama of default and restructuring. But debt is also reduced through financial repression, a tax on bondholders and savers via negative or below market real interest rates. After WWII, capital controls and regulatory restrictions created a captive audience for government debt, limiting tax-base erosion. Financial repression is most successful in liquidating debt when accompanied by inflation. For the advanced economies, real interest rates were negative ½ of the time during 1945–1980. Average annual interest expense savings for a 12—country sample range from about 1 to 5 percent of GDP for the full 1945–1980 period. We suggest that, once again, financial repression may be part of the toolkit deployed to cope with the most recent surge in public debt in advanced economies.

Don’t worry if you read that and glazed over immediately, it will make sense in a moment.

If you have a too much debt as an individual, and don’t have the ability to pay it off, you're likely going to default on the debt. However, a country whose debt is denominated in its own currency has 2 advantages. Firstly, it can simply print more money to pay off the debt by issuing more bonds and getting the central bank to buy them. Secondly, it can keep interest rates artificially low so that the cost of servicing the debt is kept low. By printing more money like this, the government will also create inflation, which will decrease the value of the debt.

Debt denominated in its own currency means that it has borrowed money in its own currency. For example, the UK government borrows pounds, by selling bonds for pounds. You may think that all countries should be able to do this, but this is not typically the case with developing countries. Many entities will refuse to lend to a developing country in its own currency, as it has a higher risk. For example, Indonesia has lots of debt denominated in dollars. If the Indonesian government tries to print their native currency to pay off this dollar-debt, they will devalue their currency relative to their debt and actually make it harder to pay off.

Here is the UK government debt from 1930 until 1970. Even though debt-GDP came right down after WW1 and WW2, the debt never actually came down.

The reason for this is because GDP increased in part from actual economic growth, but also simply from inflation. As GDP is simply the market value of all the final goods and services produced and sold in a quarter or year by a country, when there is inflation, the cost of goods and services increases, which also increases GDP. By printing more money, governments can essentially inflate the debt away.

Typically, interest rates should move with inflation, so that at least savers can keep up with inflation by holding bonds which pay them a yield. When interest rates are higher than inflation, it is called a positive real interest rate.

Real interest rate = Yield on a bond - Inflation rate

What the IMF paper details, is the method of keeping interest rates on bonds below inflation, so that real interest rates are in fact negative. This decreases the cost of servicing the debt and makes it even easier for inflation to do the work in devaluing the debt. They call this financial repression.

debt is also reduced through financial repression, a tax on bondholders and savers via negative or below market real interest rates.

For the advanced economies, real interest rates were negative ½ of the time during 1945–1980.

This is how the debt was brought down so much from 1945-1980. The paper then states that by keeping real interest rates negative 1/2 the time, governments saved about 1-5% of GDP every year for the full period. A great outcome for the government, and less so for people’s savings. The sad outcome of this is that it is the lower income individuals who suffer the most as they typically hold most of their savings in cash at a bank, not in hard assets like property, gold or stocks which will hold their value better.

Average annual interest expense savings for a 12—country sample range from about 1 to 5 percent of GDP for the full 1945–1980 period.

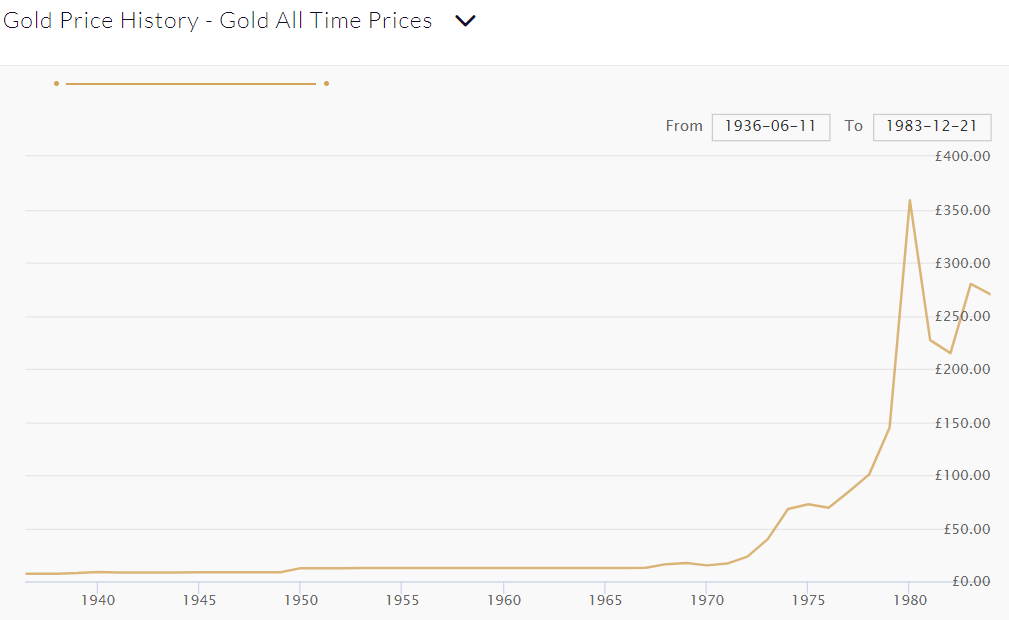

If we look at the buying power of the pound in this period, we can see that a £100 in 1945, would only buy you £10 worth of goods in 1980.

Whereas gold in contrast held its value much better, especially after the gold standard ended in 1970.

So, to answer question one, governments brought down debt-GDP by increasing the supply of money to let inflation erode the debt away, and by keeping interest rates below the inflation rate for about half of the time.

Why is the Fed raising rates so much with debt-GDP this high?

The Fed is raising rates so much with debt-GDP this high, simply because inflation is so high.

After printing trillions during Covid, central banks all around the world said that any inflation would simply be transitory (i.e. not last very long). As I’m sure you have all noticed, they were all very wrong. They are now desperately trying to regain credibility, by bringing inflation back down through raising interest rates.

How do rising interest rates bring inflation down?

When interest rates are low, it’s cheap for individuals and businesses to borrow money in order to buy assets or start businesses. This increases demand for goods and services. For example, you decide to take a mortgage out to buy a bigger house, which requires more furniture, more heating, possibly more repairs etc. This is all done with borrowed money which did not exist before you took out that loan, so there is essentially more money chasing the same amount of goods which causes a rise in prices.

The opposite occurs when interest rates rise. It’s more costly to start a business with debt and it costs a lot more to take out a mortgage. This leads to less people taking out loans and many individuals and businesses could actually default, resulting in unemployment. Generally, everyone has less paper currency to buy things with. As there is now less money chasing the same amount of goods and services, the cost of those goods and services decreases. All this typically results in a recession, which we are seeing played out right now.

With inflation around 8% in most western countries, central banks are ramping up interest rates to try and bring it back down.

Therefore, the answer to question 2 is that the Fed is raising interest to decrease demand in order to bring down inflation, which will likely result in a recession.

Can governments afford to raise rates with debt-GDP so high?

The answer is that it depends on what inflation is doing.

If inflation is high, then governments can afford to raise rates, as long as they are kept below the rate of inflation (negative real interest rates = decreasing debt-GDP). There may be times when interest rates are briefly higher than inflation, but the governments will be unable to sustain this for long.

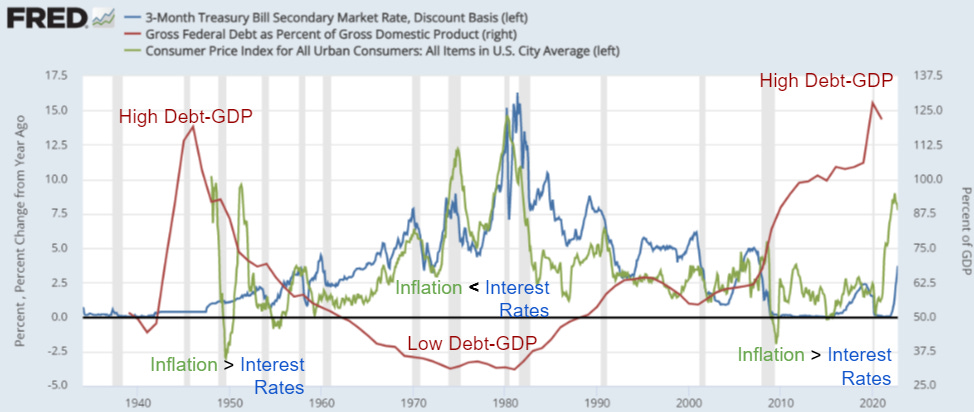

We can see this below, in both the 1940s and 2010 up till today, you rarely ever see interest rates above inflation. On this chart I have plotted the Debt-GDP (red), interest rates in blue, inflation (green) and the grey vertical lines show recessions.

We can see that in the 40s and early 50s, when they had debt-GDP at levels like we have today, inflation (green) was significantly higher than interest rates (blue) for most of the period and the same can be seen in the period from 2010 to today. Even though they have raised interest rates significantly, it still remains far below inflation. In contrast, during periods where debt-GDP was much lower like the 80s and 60s, even with inflation very high, interest rates were often still higher than inflation.

I think the above chart really captures the larger picture beautifully. It paints the environment that central bankers are working with and what their limitations are. They are dancing a dangerous dance of trying to bring down inflation, whilst simultaneously needing it to help bring down debt-GDP. The largest risk is that we get too much inflation with too much money printing, which can lead to a collapse of the fiat monetary system, like what happened in Weimar Germany.

What does this all mean for the average Joe?

And finally, what does this mean for people like you and me.

In the short term it means of downward pressure on assets, like we have seen over the last year. Pretty much all liquid assets have suffered, and housing prices will continue to roll over, as we are already starting to see. So long as the central banks keep ‘draining’ money out of the system to try and fight inflation, it’s difficult for any assets other than cash to do well.

In the long run, the unfortunate likelihood is that it the next 5-10 years is likely to be somewhat less prosperous than the last 40 years. As people get more frustrated with their stagnating or decreasing living standards and struggle to make ends meet, populist movements will gain more popularity, which we are already seeing today. I would expect this lead to see some pretty strong swings in politics to both extremes. In particular, I think we could see a strong rise in socialist movements, as the wealth gap becomes so huge, and more people will look at the rich in distaste as they struggle to make ends meet.

In terms of how to protect yourself during such times, the answer is simply diversification and cutting excessive spending.

Owning a range of hard assets is the only way to protect against devaluation of currency. Hard assets include real estate, land, gold, Bitcoin and stocks. Owning all of these is not necessary, but you need to hold some.

Real estate when combined with a 30-year fixed rate mortgage at a low interest rate is optimum, as money printing increases the value of property and decreases the value of the debt.

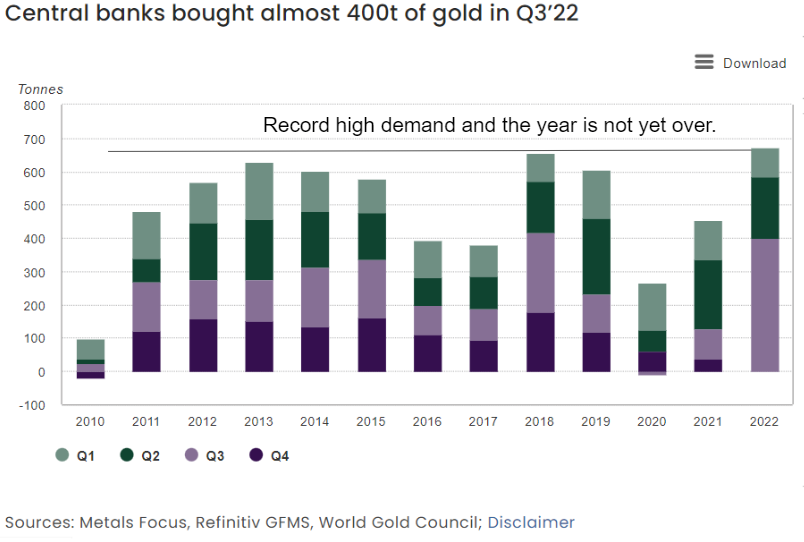

Gold is dismissed by pretty much everyone but owning some in the form of a simple ETF of Gold Miners ETF seems a no brainer. Central bankers have been buying at the highest rate in the last 12 years, whilst retail have mostly been selling. Gold is simply a hard asset like Bitcoin, except it’s large enough for central banks to want to own it. Whether or not Bitcoin eventually replaces gold doesn’t really matter, because you don’t know anything for certain, so you should always hedge your bets.

Holding Bitcoin is also a no brainer. It’s the only asset you can easily self-custody (not keep on an exchange or in a bank), you can literally buy £1 worth of it, and it is currently pretty cheap when looking at the big picture. I don’t expect a bull run until 2024/2025, but I will be buying more over the next year in preparation.

With stocks you ideally want to avoid expensive high growth tech stocks with no actual revenue. The safest bet is to own a mixture of ETFs, like value, dividend, commodities, and regular index funds. Don’t bother trying to pick individual stocks, unless you can be bothered to do a lot of homework.

Index funds are funds which invest in every company in a given index. The S&P 500 is the most popular US stock index, so if you buy an S&P 500 index fund, it simply invests in every company in the index.

Then as a safety net against any volatility you want a good portion of cash. Having cash allows you to invest when others are panic selling or capitulating and makes you psychologically indifferent to crashes. When you have a good portion of cash, bear markets simply represent good buying opportunities, not something to fear.

If you don’t have any savings in the first place, it’s probably a good time to try and build some. Try not to spend excessively and perhaps try to increase your income with a small passionate side hustle. Lyn Alden had a great article on the topic which you can read here.

And most importantly of all, be healthy, have cold showers, read books, spend time with friends and maybe grow some vegetables or keep some chickens if you can. And remember, nothing stays the same forever. Following every crisis is a time of peace and resolve.

What will be, will be…

Crypto Carnage

I can’t send this newsletter out without touching on the recent drama in crypto land.

FTX, the world’s 3rd largest crypto exchange, is now insolvent.

Yep. Pretty major. What’s more major, is the manner in which things went done.

Let’s dig into it.

Sam Bankman-Fried’s first venture, was a wildly successful crypto hedge fund which he founded after he started arbitraging the Japanese Bitcoin premium. The hedge fund was called Alameda Research.

After the arbitraging opportunities dried up, Alameda pivoted to become market maker and made massive sums of money using quantitative trading strategies. It earned a reputation of exceptional returns and a less sterling reputation for quietly dumping crypto tokens on retail.

One example is Stargate.

Hugely hyped and they claimed they wouldn’t sell any token for at least three years. Shortly after, they secretly sent 8.4M Stargate token to FTX and Binance.

Startgate is down from $4.14 to $0.42. A classic VC dump, which is sadly all too common in crypto.

FTX was then founded after Alameda and was branded as a platform “for traders, by traders.”

Given that FTX was an exchange, and Alameda was a hedge fund, there has always been lots of speculation on the relationship between the entities and what dodgy business might be going on.

The rumours were that FTX gives Alameda priority orderflow, allowing the hedge fund to front-run traders and give them an advantage.

FTX rose up to become the 4th and sometimes 3rd largest exchange in the world and became the perfect source of money for Alameda’s trading operations.

Where things start to go wrong is on November 2nd.

CoinDesk wrote a news story claiming to have acquired Alameda’s balance sheet. It showed that $5.8 billion of the $14.6 billion reported, were all in FTX’s own exchange token, $FTT.

A large majority of the rest were all in Solana ecosystem tokens.

Exchange’s give their tokens utility by offering discounted trading fees, access to airdrops, free withdrawals and VIP access, incentivising users to hold the token.

In addition, 1/3 of FTX’s own revenue was used to purchase and burn $FTT token, decreasing the supply and helping ‘number go up.’ Sam would even post twitter posts of him buying $FTT weekly.

The dodgy part is that $FTT has a remarkably low circulating supply relative to Alameda and FTX’s holding. Alameda’s holdings represented 2-3x $FTT’s circulating supply. This means that if Alameda ever tried to sell the $5.8 billion worth of FTT, there wouldn’t be enough buyers and they would push the price of the token down to near 0.

Circulating supply of a token is how much of that token are publicly available and are circulating in the market.

This strategy of having a low circulating supply, but a high total supply kept by the company or institutions, is rather common to most Solana ecosystem token and the ones present on Alameda’s balance sheet. This means that although it looks like they have a lot of assets, if they actually tried to sell any of them, they would be unable to sell them all as they would push down the price so much.

Here are two tokens that are like this. Look at how small their market caps are relative to the fully diluted market cap (factoring in all the token which exist but are not available to the public).

What’s wild is that Sam himself describes much of Defi and crypto as simple ponzi schemes, which much of it is, but pretty crazy coming from one of the Kings of crypto.

With FTX, the $FTT token, and Alameda setup they can really get down dirty with the business.

FTX creates $FTT token

→ Alameda buys or pre-mines them at a super low price

→ FTX does some great marketing and pumps the $FTT token

→ Alameda then deposits their now highly valued $FTT token and uses it as collateral to borrow money from FTX

→ FTX lends out assets from FTX’s customer deposits.

What could possibly go wrong…?

Both entities can show auditors they have legitimate credit agreements and claim a genuine arms-length relationship.

The stability of this relationship hinges on the price of $FTT and customers not withdrawing their assets from FTX exchange.

If $FTT were to start crashing, Alameda would need to post more collateral for their loans, and if customers start withdrawing money from the exchange, FTX needs to scramble to get its customers funds back from Alameda or find additional funding to give funds back to customers.

Then a few days later, some analysts on twitter noticed a large transfer of $FTT tokens onto Binance. There was some wild speculation that Binance was selling their $FTT holdings.

Then on November 6th, CZ, head of Binance tweets this:

Boom.

For the CEO of Binance, the world’s largest exchange, to publicly and announce he is selling all of your token is brutal and is of course going to lead to a lot of selling pressure.

Caroline, the head of Alameda then offers to purchase the $FTT token in a straight swap between the two for a price of $22 to reduce price impact.

Why $22? It’s a key level of support.

Strangely, CZ declines the offer.

It is strange because he would have been able to sell his $FTT for a higher price, because his announcement and selling will push the price of $FTT much lower than $22.

The ensuing sell pressure pushed $FTT below $22 around 8pm EST and by the next morning, FTX had paused all withdrawals of user funds from their exchange.

Before freezing withdrawals, Sam tweeted this now deleted tweet:

Now this is where things get even wilder.

Sam and FTX are in desperate need of funding so that they can process customer withdrawals. They get rejected by everyone, and with nowhere left to turn, CZ steps in and buys the entirety of FTX. The key part of the agreement is that CZ is allowed to back out of the deal at any time if they deem FTX too bad to save.

Low and behold, the next day Binance announced they are backing out of the deal and letting FTX burn.

And a few days later FTX filed for bankruptcy.

Not only was FTX one of the largest exchanges, Sam was also a darling of the regulators and spoke numerous times in congress. He was also the second largest donor to the Biden administration and was often coined the JP Morgan of crypto, as he claimed to have so much money which he used to acquire BlockFi and Voyager, a crypto yield platform and exchange.

The knock-on effects are likely going to be pretty huge, and it remains unclear who else will suffer from the contagion. This is good in the long-term, as it washes out dodgy dealings, but it will still be painful for crypto, especially the institutional side. Although it can lead to some downward pressure on Bitcoin, I think it’s worse for general crypto and the world of altcoins, both from the institutional interest side and the regulation side.

The key takeaway for individuals is to take any Bitcoin or crypto you have off exchanges.

‘Not your keys, Not your coins’ has never been more important, and until all this settles over, you don’t want to risk holding crypto assets on any exchange.

Crypto.com and Kucoin are both rumoured to be in slightly dodgy positions, so be sure to get off them.

Here is a good short thread, from one of CowSheds speakers, on how you can take your Bitcoin off an exchange:

And creds to this guy for the excellent summary of events:

Bitcoin

I shared this chart in the last newsletter as a possible path Bitcoin could take:

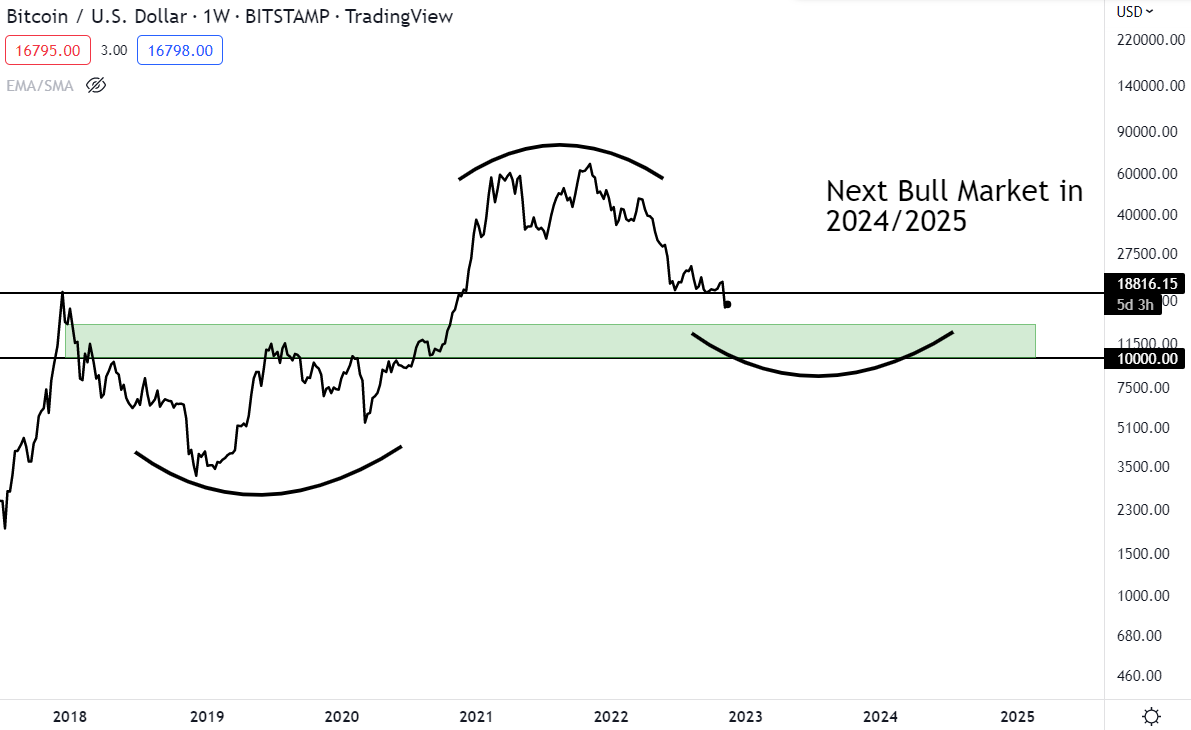

And it seems Bitcoin is intent on mimicking the path of previous bear markets. This is how it looks today:

We are currently breaking down from a key level of support, and it seems likely that we shall eventually dip into the green region to start forming a cycle bottom.

My longer-term, rough view, is that we will probably start forming a long-boring bottom in this region, setting itself up for a bull market sometime in 2024 or 2025.

I won’t touch on all indicators in this edition, as nothing has significantly changed, and it has already been a fairly long newsletter.

The play of the game remains the same. I still view dollar cost averaging as the best way to gain exposure to Bitcoin, and I wouldn’t touch altcoins with a barge pole in this environment, which is something I’ve been saying all year.

Dollar cost average (DCA) means investing incrementally in small amounts, typically monthly or weekly.

If you do wish to buy some Bitcoin, you can get £10 worth of Bitcoin for free by setting up a Luno wallet and using the code BPTATSUKI in the rewards section. Although I wouldn’t keep any crypto on any exchange, you still need to buy it from an exchange, and Luno have been doing a full proof-of-reserves since last year, so it’s a safer bet than most.

Once you’ve done that, you can go ahead and book a free webinar by Jason Dean, a great guy who I met at a Bitcoin conference in Edinburgh, who I will be interviewing in a podcast tomorrow! It’s a good high-level beginner overview of all the basics, and if you are fairly new to Bitcoin I recommend you sign up.

Jeff Booth had a great line in which he said he no longer tells people to buy Bitcoin, he simply tells them to go away and learn about it.

This webinar is a great way for you to do just that.

I’ll end by sharing the short essay on Chamomile that my good friend sent to his tinder date: The Chemistry of Chamomile

Maybe you will have better luck in securing a date with it…

Have a great day, and don’t hesitate to drop a question or feedback in the comment section below.

All the best,

Tatsuki

Library

Bullish - Causing, expecting, or characterized by rising stock market prices.

Bearish - Causing, expecting, or characterized by falling stock market prices.

Bear Trap - Tricking everyone that price is going to break down, before moving up.

Bull Trap - Tricking everyone that price is going to break up, before crashing down.

DCA - Dollar Cost Average. Investing incrementally on fixed schedule.

DEX - Decentralised exchange.

EMA - Exponential moving average

ETF - Exchange traded fund. A type of security that tracks an index, sector, commodity, or other asset, but which can be purchased or sold on a stock exchange the same way a regular stock can.

Fed - The Federal Reserve, central banking system of the US.

Fiat Currency - Fiat money is government-issued currency that is not backed by a physical commodity, such as gold or silver.

FOMC - The Federal Open Market Committee (FOMC) is the monetary policymaking body of the Federal Reserve System.

Fractal - Repeating patterns from the past.

HODL - To hold your coins and not sell them despite crashes in price.

MA - Moving average.

S/R - Support/Resistance level.

Stablecoin - A cryptocurrency pegged to a traditional fiat currency, like the dollar.

Whale - A very large holder of Bitcoin.

The information contained herein is for informational purposes only. Nothing herein shall be construed to be financial legal or tax advice. The content of this email is solely the opinions of the write who is not a licensed financial advisor or registered investment advisor. Trading cryptocurrencies poses considerable risk of loss. The writer does not guarantee any particular outcome.

Very helpful to have some idea of what’s going on. Thank you :)